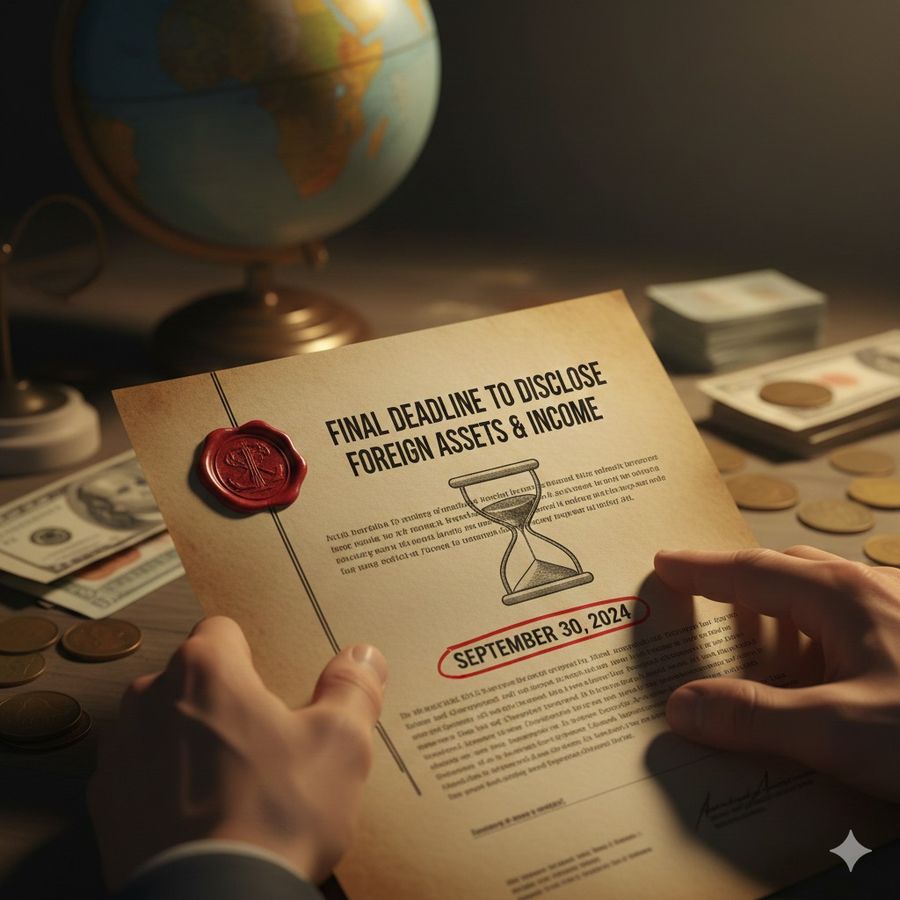

Final deadline to disclose foreign assets and income

The final deadline to declare foreign assets and income is approaching. Failure to disclose may result in penalties or legal consequences. Ensure all relevant information is accurately reported before the cutoff to comply with tax regulations and avoid complications. This is the last opportunity to submit your disclosures.

As the deadline for declaring foreign assets and income rapidly approaches, taxpayers are urged to take immediate action to ensure full compliance with tax regulations. Authorities have reminded individuals and entities with overseas holdings that failure to disclose relevant information by the final cutoff date may lead to significant penalties or legal consequences.

Represents the last opportunity for taxpayers to come forward and declare any foreign accounts, investments, real estate, or income earned abroad. This applies to residents and citizens alike who have financial interests outside the country that have not yet been reported through official channels.

Tax authorities emphasize that transparency is crucial in the fight against tax evasion and money laundering. Accurate reporting of foreign assets helps maintain the integrity of the tax system while ensuring fair revenue collection. For individuals with complex or multiple overseas investments, it is advisable to review all financial records carefully and consult with tax professionals to avoid errors or omissions.

Failure to comply with the disclosure requirements can trigger severe repercussions. Penalties may include substantial fines, interest on unpaid taxes, and in serious cases, prosecution that could result in imprisonment. Additionally, undeclared foreign income or assets uncovered during audits may retrospectively be subject to taxation under more stringent terms.

The government has made various efforts to facilitate the disclosure process, including online submission platforms and informational resources explaining the types of assets that must be reported. Examples of reportable foreign assets include foreign bank accounts exceeding specified thresholds, ownership in foreign companies, foreign securities and bonds, and real estate held abroad. Income from these assets, such as dividends, rental income, or capital gains, must also be reported.

Taxpayers are encouraged to act promptly and submit their disclosures ahead of the deadline to avoid last-minute complications or system overloads. Late submissions may still be accepted but could attract additional penalties or reduced leniency.

In summary, this final deadline marks the last chance for taxpayers to bring their foreign financial interests into compliance with national tax laws. By ensuring all foreign assets and income are accurately declared, taxpayers can avoid legal issues and contribute to a fairer tax system. For further assistance, consulting certified tax advisors or accessing official tax authority resources is highly recommended.

Don’t wait until it’s too late—declare your foreign assets and income now to stay on the right side of the law.